GENERAL TRENDS

Industry Outlook and Observations

In 2025, commercial property maintenance and multi-trade facility services remained a resilient “non-discretionary” spend category driven by asset uptime, safety/compliance, and cost control—supporting continued outsourcing and consolidation activity.

North America market size: estimates place the North America facility management market at ~$456B in 2025, forecast to reach ~$532B by 2030 (~3.1% CAGR).

2025 buyer priorities increasingly centered on cost efficiency and operating reliability, with a strong push toward vendor consolidation and tech-enabled service delivery. JLL characterizes FM as a “$3 trillion” global industry, noting 84% of CRE/FM leaders cite escalating operating costs/budget constraints as the top concern.

Recent and Upcoming Trends

Vendor Consolidation + Bundled Scopes (2025 → 2026+)

Customers increasingly prefer fewer partners that can cover preventative maintenance + break-fix + compliance documentation, supported by portfolio reporting.

JLL specifically highlights consolidating contracts/suppliers and prioritizing providers with integrated/self-delivery capabilities as a leading cost-reduction approach.

AI + Data-Powered Operations (accelerating into 2026+)

In 2025, AI adoption moved beyond experimentation: 28% of organizations have embedded AI in FM operations (rising to 46% for very large organizations).

Expect 2026+ competitive separation around: faster dispatch, better triage, tighter closeout documentation (photos/notes), and predictive maintenance—especially for multi-site portfolios where reporting standardization is valuable.

Labor Tightness in Skilled Trades (persistent 2025 reality; 2026+ constraint)

The skilled trade labor market remained tight in 2025, driven by demographic attrition and sustained demand across maintenance, construction, and infrastructure. Labor availability is expected to remain a structural constraint in 2026 and beyond.

Providers with strong recruiting, training, utilization, and route density are better positioned to maintain service levels, protect margins, and gain share.

Reliability / Mission-Critical Standards “Spill Over” into General Commercial Maintenance

Business continuity is the foremost risk priority for mission-critical environments (e.g., data centers, hospitals, labs), pushing higher expectations around resilience planning and uptime.

Even outside mission-critical, many owners are adopting stricter SLAs and documentation norms learned from those environments.

M&A Catalysts

Fragmentation + roll-up economics: route density, centralized dispatch, standardized KPIs, and procurement-driven vendor consolidation continue to favor platform strategies.

Cost pressure drives outsourcing: Strong push toward outsourcing/streamlining supply chains as a cost-reduction lever.

Demand for integrated capabilities: acquirers continue to buy breadth (multi-trade, compliance, specialty) to win “single-vendor” contracts.

Technology as a differentiator: platforms acquiring businesses with strong systems and reporting discipline (or quickly upgrading them) will outperform.

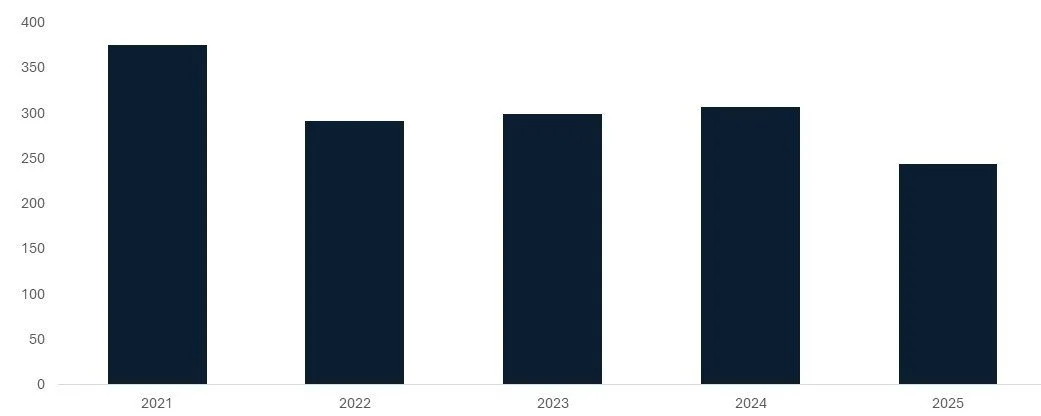

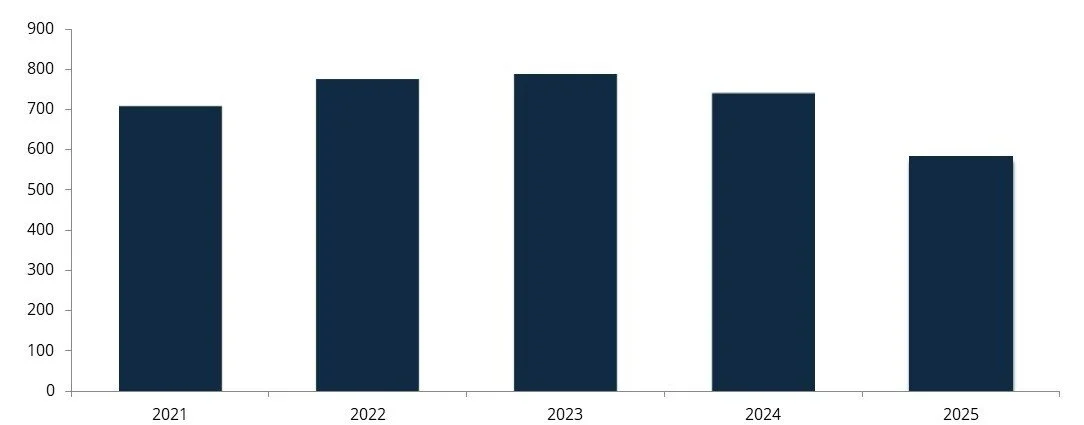

M&A ACTIVITY

North American Facility Services Transaction Velocity

DEAL SPOTLIGHT

Date: January 2025

Target: Advanced Facility Solutions (AFS)

Buyer: Persona-Triangle (Exeter Street Capital Partners / Patriot Capital Group affiliate)

Transaction Value: NA

Strategic Fit:

The acquisition strengthens Persona-Triangle’s position as a scaled, multi-site facilities services platform by expanding geographic reach, service density, and customer coverage.

AFS adds recurring maintenance relationships and coordinated service delivery capabilities that align with customers’ preference for vendor consolidation and single-point accountability.

Expected Outcome:

The combined platform is expected to benefit from increased route density, improved technician utilization, and broader cross-selling of preventative and reactive maintenance services.

The transaction supports a continued buy-and-build strategy focused on recurring revenue, operational leverage, and enhanced enterprise value.

Date: April 2025

Target: Kept Companies

Buyer: DFW Capital Partners

Transaction Value: NA

Strategic Fit:

Kept’s recurring service model, national footprint, and dense route structure align with private equity demand for predictable cash flow and operational scalability in facilities services.

The business benefits from long-term customer relationships and standardized service delivery across large portfolios.

Expected Outcome:

Under new ownership, Kept is expected to continue expanding through organic growth and tuck-in acquisitions, leveraging centralized systems, labor optimization, and procurement efficiencies.

The platform is positioned to benefit from ongoing outsourcing trends and consolidation within commercial facilities maintenance.

CLICK HERE FOR 555 RELATED TRANSACTIONS

ABOUT 555 CAPITAL ADVISORS

Investment bank and advisory firm providing bespoke M&A, capital raise, and related services to middle market companies

Transactions: 100% Sale or Divestiture, Growth Capital, Recapitalizations, Mergers, Management Buyouts, Acquisition Advisory and Financing

Industries Served: Manufacturing, Business Services, Consumer, Technology, and Healthcare

Highly experienced and personalized client relationships: 25+ years experience, 100+ transactions, and mandates, customized solutions

The opinions expressed herein are those of 555 Capital Advisors. There is no guarantee that any predictions/projections as to certain market activity or events will come to fruition or past market or transaction performance referenced within will yield the same results as transactions previously conducted by 555 Capital Advisors.

Securities offered through Finalis Securities LLC Member FINRA & SIPC

This presentation contains information obtained from third parties, including but not limited to market data. 555 Capital Advisors believes such information to be accurate but has not independently verified such information. To the extent such information is obtained from third-party sources, there is a risk that the assumptions made and conclusions drawn by 555 Capital Advisors based on such representations are not accurate.